Continuous Contracts Explained

The Concept

Let's

begin with a futures market - Soybean Oil, or Soyoil for short - and say

that there is no such thing as a continuous series of Soyoil futures

prices. Futures markets are comprised of individual contracts, each with a

pre-determined life-span. At any stage, the market consists of a

number of contracts, or "delivery months", that have expiry dates

stretching out into the future. As one contract expires, another is listed for trading, and so the cycle

continues. The only way that a long-term continuous

history of Soyoil prices can be examined is to access a record of cash

market prices. Of course, it's always possible to

"splice" the individual Soyoil futures contracts together in

some way, so as to represent their history. But it must be borne in

mind that the result will merely be a representation of that

history, or a computation, that is handled by a particular

algorithm.

Splicing contracts together

If

all delivery months in the Soyoil cycle were "equal", it would

make sense to splice them together by a very simple algorithm: "when

one contract expires, begin to display the next". This type of series

is called a "spot-month continuous". But delivery

months, particularly in commodity futures markets, are generally not

equal. The delivery months that the Chicago Board of Trade offers for

Soyoil trading are intended to cover the underlying agricultural cycle so

as to give industry participants full scope to hedge their specific needs.

They are not spread equally through the calendar year. For instance, there

is a sequence of contracts expiring in July, August, September and October

and then a jump to December. A hedger may not be interested in the

August, September and October contracts at all, and may prefer to trade in

the December contract well before any of the intervening contracts have expired.

Trading volume tends to be spread unequally between different delivery

months. Sometimes an exchange introduces a new delivery month into a

market cycle and the

industry completely ignores it. The same disinterest may be shown by

a speculator. He may have his own reasons for trading December Soyoil

"early" in the cycle. For instance, he may be discouraged by the

necessity of "rolling" through all of the intervening

contracts, incurring commission costs and potential "slippage"

each time. If the trading volume is sufficient to allow it, why not just

jump straight into December? The "spot-month"

continuous contract - how useful is it? It is often assumed

that a continuous contract has to display the "spot month" at

all times in order to be "correct". This is not the case. A

continuous contract is a representation and that representation is correct

only in so far as it is useful. There is no single "correct"

way to compute a continuous contract for any futures market. The

"spot month" representation is probably the most popular, but

not necessarily the most useful. To understand why,

let's consider Silver. An examination of the trading volumes in Silver

futures reveals a marked decline from about a month before the expiry of

each delivery month (see table below). This decline coincides with First Notice Day. If a

trader remains in a contract after First Notice Day, he is at risk of

having to take delivery of the underlying commodity. A Silver

contract still has a month to run after First Notice Day, but very soon

only a handful of industry participants will be trading it. Is there any

use in incorporating the last month of Silver prices into a

continuous contract if that portion of the delivery month will never be

traded? There might be, if no other prices were available, but current prices are

always available from any of the subsequent delivery months. It might be argued that the

spot month prices are the most

important from an "overall analysis point of view". This

argument amounts to saying the following: "My next trade will be in

October Cotton. But I shan't look at prices from the October contract,

even though I am able to. I shall continue to study July prices, because

July is the spot month, and it still has a fortnight to run." This

argument becomes especially curious when it is considered that the July

and October Cotton contracts virtually cover different crops! Rolling on

Volume and/or Open Interest Another simple algorithm for

constructing continuous contracts is to follow the market's lead.

When volume and/or open interest become larger in a back-month, the series

leaves the current contract and moves to the back-month. On the face of

it, this is a clever algorithm, as it automatically circumvents

liquidity problems. It may also surmount the Notice Day problem, by

assuming that trading volume always leaves the current contract in time. The

trouble with the algorithm is its over-riding assumption - that liquidity

is the only appropriate criterion for selecting delivery months. Let's consider

the Eurodollar contract, which is one of the most heavily traded in the

world. There is reasonable volume in at least the first 12 listed

quarterly contracts. Furthermore, there

will often be little difference between the nearby quarterly contract and the

next one out in terms of volume - the volume and open interest will be huge in each. This

invites an obvious question: if the contract with the greatest volume is

the "correct" one to be following, why is there so much interest

in the others? The answer is that different delivery months offer

different trading opportunities, both for hedgers and speculators. The

Eurodollar futures market attempts to predict the level of interest rates

on Eurodollar deposits at specific times into the future. The closer

that the time is to "now", the more sensitive the market is to

what happens to cash rates. Because of this, prices in different

delivery months can move in contrasting manner. For instance, prices in

the spot month may move quite sharply while back months remain relatively calm,

and

vice versa (see charts below). It is even possible for prices in one month to go up and in

another down, although this sort of divergence is most common in commodity futures markets,

where seasonal factors play a larger role. The assumption that all

delivery months are homogenous, which is implicit in the volume/open

interest algorithm, is mistaken, at least for most types of futures

markets. This is easily demonstrated if different roll schedules

are used to construct continuous contracts for the same market. The

variation in the results is often quite apparent to the naked eye. Some system traders are

happy for their continuous data to be "handed" to them by an

algorithm such as rolling on volume/open interest. Others prefer to

construct their own data and experiment with the results. Rolling on volume and/or

open interest is a good way to construct continuous contracts, as long as

the question of which delivery month appears in the series at any time is

not considered an issue.

Part 2 of the article looks

into a problem with simple "spliced" contracts and introduces

"back-adjusted" contracts.

Click on

Part 2 to continue.

Illustrations

1)

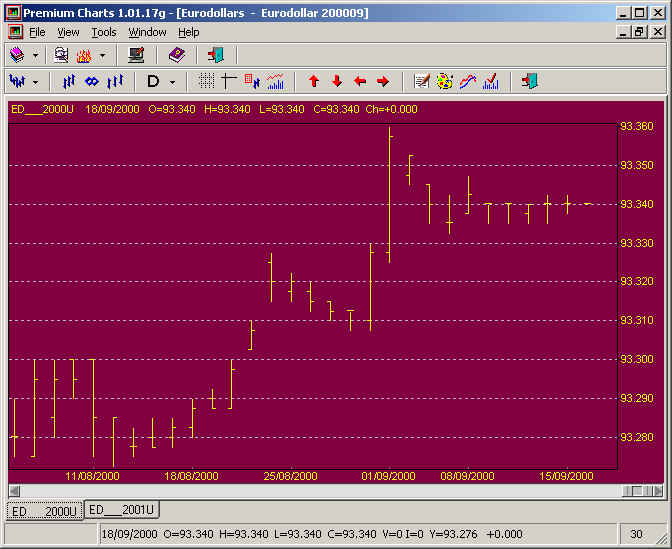

The

first chart below show the September 2000 Eurodollar contract trading

through a 9-point range in the final 30 days of its life. 2)

At the same

time, the September 2001 Eurodollar contract was trading through a

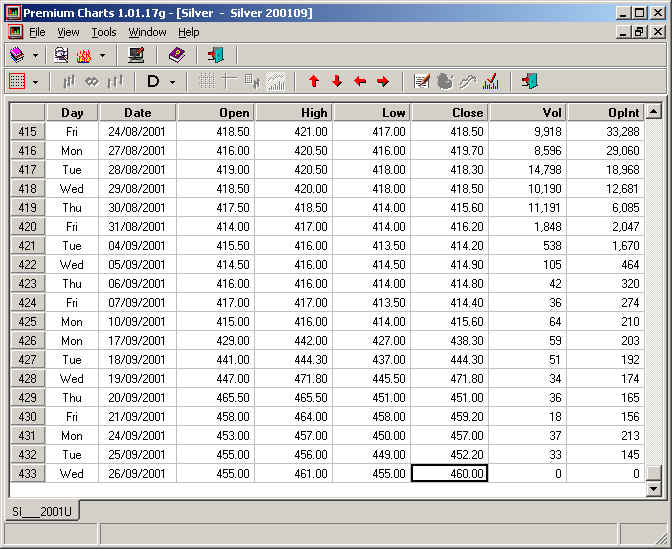

39-point range. 3) The table shows volume and open

interest in the September 2001 Silver contract falling away rapidly towards expiry.

Part 2 of the article looks

into a problem with simple "spliced" contracts and introduces

"back-adjusted" contracts.

Click on

Part 2 to continue.

|