Continuous Contracts Explained Part 2

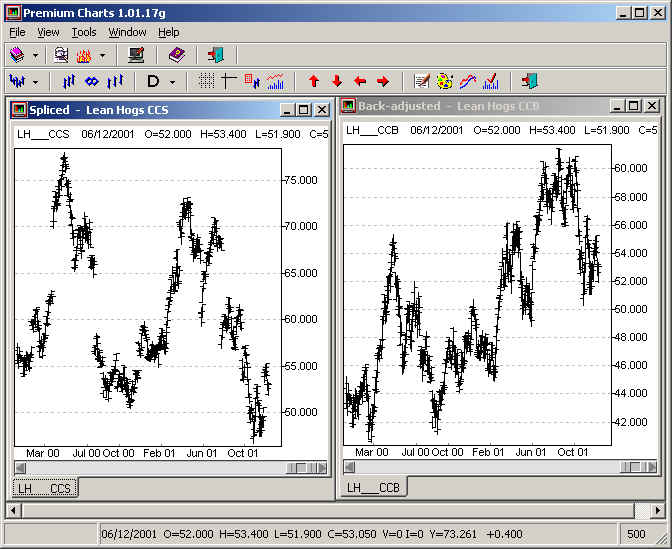

The chart below shows two years of a spliced continuous contract for

Lean Hogs. The most obvious thing about the chart is that it tends to

consist of "clumps" of data separated by large gaps. What are

these gaps and where do they come from?

The

Problem with Simple "Spliced" Contracts

In Part 1

of this article, it was argued that the different contracts in a futures

market are not homogenous. Each delivery month points to where cash prices

might stand at a particular date in the future. Therefore each contract will tend to

trade at its own level. This leads to a problem when individual contracts

are spliced together. When one contract is replaced in the series by

another, the difference in price between the two will manifest itself as a

gap. This explains the gaps evident in the Lean Hogs chart above. For

instance, the first big gap in the chart, when prices appear to

"jump" from around 62.5 to 70 early in 2000, was caused by the

following sequence of events: 23/3/2000 - the April 2000 contract closes

at 62.525. It is now abandoned.

On the same day, the June 2000 contract closes at 69.950

24/3/2000 - the June 2000 contract, which is now the current

contract in the series, closes at 70.525. The spliced chart suggests

that the Lean Hogs market jumped about 7 basis points from the 23rd to the

24th. But the June contract itself jumped only 1.25 points. It was already

trading well above the level of April on the day that April was abandoned.

So when did the market jump those 7 points? The answer is that it never

did. The "market" is actually comprised of individual contracts

that run their own course. The spliced continuous contract attempts to

represent the longer-term history as best it can, but given the spurious

gaps that it creates, there are obvious limitations as to what a spliced

contract can achieve. What is a spliced contract good for? The

spliced contract offers a

"staccato" version of futures prices, with discontinuities

evident. Nevertheless, it can be used to identify where futures prices have

traded in the past. It paints the picture with a broad brush, but a

spliced chart can give a good idea of whether current futures prices are

high or low in an historical sense. What is it not good for? Any

numerical price indicator run on a spliced contract will reflect the

discontinuities inherent in the series. For instance, a moving average

will jump along with every gap. To the extent that an indicator is used to

assess market sentiment, it will provide a false reading, because the gaps

in a spliced contract are not caused by market activity. A spliced

contract will distort the testing of trading systems. Unless instructed

otherwise, a computerised system test based on a spliced contract will

incorporate the price gaps as evidence of profit or loss. What

is the solution? The answer is simple - take the gaps out!

The

Back-Adjusted Continuous Contract

In a

"gap-adjusted" continuous contract, every price gap caused by a

contract "roll" is measured and removed. The procedure can work

in either of two ways: it can start at the beginning of the series and

work its way forwards, removing each gap in turn, or it can start at the

end and work its way back. The "back-adjusting" method is

preferred, because it leaves current prices intact. Only those prices

prior to the last roll date are adjusted. So how is the

roll gap measured? The simplest way is to compare the closing prices on

the roll day. Using the example from above, we have: 23/3/2000 - June

Lean Hogs - 69.950

23/3/2000 - April Lean Hogs - 62.525

Roll gap = + 7.425 The roll gap is "up". How do we make it

disappear? We can't do it by magic. What we have to do is adjust all

previous prices up by 7.425 points. This effectively

"closes" the gap. Here is the back-adjustment algorithm in a

nutshell: working our way backwards, we measure every roll gap and adjust

all previous prices up or down according to whether the gap happens to be

positive or negative. The gaps are now eliminated. Of course, this

process never ends, a point that needs to be emphasized: every time a

new contract is added to the series, the back-adjusted contract is

re-calculated and all previous prices are adjusted. Now let's have a look at the

result. The original spliced chart is shown on the left and the

back-adjusted version appears on the right.

Misconceptions about back-adjusted contracts Many

traders are happy to see spurious price gaps removed from their continuous

contracts but are unhappy with the result. They complain that the

back-adjusted prices are not "real", often citing the fact that

in some contracts the historical prices are actually negative. Traders looking for real

historical prices should consult their spliced charts. Prices in a

back-adjusted series are adjusted deliberately, so the complaint

about "unreal" prices misses the point. Gaps in a back-adjusted contract

disappear because historical prices are altered.

There is no other way to do it. Trading reality versus historical price reality If the prices in back-adjusted contracts are mostly

spurious, then of what use are they? To answer this question, let's

imagine that we enter a position in Lean Hogs on the first day in the

series and hold it to the end, rolling the position forward from one

delivery month to the next. If we ignore commission costs and execution

"slippage", the back-adjusted chart can be used to calculate the

exact value of the position at any time. Back-adjusted contracts represent

a different type of reality - trading reality. They show exactly

what would have happened to a trader who held a continuous position in any

market. Therefore back-adjusted contracts constitute the perfect resource for computerised system tests. Looking at the Lean Hogs charts

above, we can say that the broad price trend in the underlying commodity

has been down, but that the trend of trading activity in the futures

marketplace has been up. Spliced contracts may be

differentiated from back-adjusted contracts as follows:

-

Spliced contracts show price levels in a futures market. As a

drawback, they also display price movements that are spurious

(price gaps that are

unrelated to trading activity).

-

Back-adjusted contracts display price movements in a futures market that are due to trading

activity. As a drawback, they also show price levels that are spurious.

Is there a third way? The short answer is "no". If

roll gaps are left in a continuous contract, you have a

"spliced" chart. If roll gaps are removed entirely, you have a

"back-adjusted" chart. The only alternative is to remove the

gaps partially. The resulting series is caught between the other

two methods and marred by the disadvantages of both. Negative

numbers In futures markets that spend a large time in backwardation

(e.g. Crude Oil), the back-adjustment process can cause historical prices

to be pushed into negative territory. Some charting/analysis programs can

display negative numbers but can't do much else with them. This is not the

fault of the back-adjustment algorithm. Part 3 of the article looks

at how DataTools handles continuous contracts.

Click on

Part 3 to continue. |